👋Introduction

Phew! Does anyone else feel like navigating the economy in 2025 is a bit like riding a rollercoaster 🎢 in the dark? With all the chatter about potential new government policies from a Trump administration, shifting tariffs, the pinch of rising inflation, and whispers of a recession, it’s completely normal to feel a surge of anxiety. Your stomach might churn a little just thinking about it. But here’s a powerful truth: in times of uncertainty, knowledge isn’t just power—it’s peace of mind. This is where financial literacy steps in, not just as a set of skills, but as a cornerstone of your overall financial wellness and, importantly, your mental well-being.

So, what exactly is financial literacy? It’s more than just knowing how to balance a checkbook (though that’s part of it!). It’s about having the skills, knowledge, and confidence to make informed and effective decisions with your financial resources. It’s about empowerment. In a world that feels a bit topsy-turvy, understanding your money is crucial for managing your daily expenses, planning for a future that might feel hazy, and sailing smoothly through economic storms.

This post will explore why financial literacy is more critical than ever in 2025. We’ll look at the common money worries many are facing, and most importantly, provide actionable strategies and resources to help you build your financial understanding and resilience.

"Financial peace isn't the acquisition of stuff. It's learning to live on less than you make, so you can give money back and have money to invest. You can't win until you do this."

- Dave Ramsey Tweet

💸 Section 1: What is Financial Literacy and Why Does it Matter (Especially in 2025)?

Financial literacy, at its heart 💖, is the ability to understand and effectively use various financial skills, including personal financial management, budgeting, and investing. It’s about being equipped to make sound financial decisions that align with your goals and values. Think of it as your financial compass, helping you navigate the complex world of money.

But in 2025, its importance is magnified. Why?

☝️Economic Volatility:

As highlighted by Investopedia (here), periods of economic uncertainty, with concerns about inflation, policy changes (like tariffs), and potential recessions, can make long-term planning feel out of reach for many. Financial literacy helps you understand these macroeconomic factors and how they might impact your personal finances, allowing you to adapt.

☝️Inflation's Bite:

Rising inflation means your money doesn’t stretch as far. Financial literacy helps you develop strategies, like effective budgeting and smart shopping, to manage rising costs.

☝️Policy Shifts:

Potential changes in government policies, such as those that might be associated with a Trump administration or new tariffs, can impact investments, taxes, and trade. Being financially literate means you’re better equipped to understand these potential changes and adjust your financial plans accordingly.

☝️Recession Preparedness:

While no one has a crystal ball, understanding how to build an emergency fund, manage debt, and make sound investment decisions – all components of financial literacy – is key to weathering potential economic downturns.

😀The benefits are clear: improved quality of life, reduced financial stress (a big one, right?), simplified decision-making, and an enhanced sense of peace and control over your money. As Calm.com notes (https://www.calm.com/blog/financial-wellness), financial wellness means you’re not constantly stressed about money because you have a clear understanding and a sound plan.

💸 Section 2: Common Financial Challenges in an Uncertain 2025

Let’s be real, managing money can be tough even in the calmest of times. But the specific anxieties of 2025 – the “what ifs” around governance, trade, and the economy – can amplify these common challenges:

- Living Paycheck to Paycheck: When inflation is high and job security feels shaky, stretching each dollar becomes even more stressful.

- Handling Unexpected Expenses: An unexpected car repair or medical bill can throw a carefully managed budget into chaos, a fear magnified when the broader economy feels unstable.

- Difficulty Saving: With the cost of living on the rise, finding spare cash to save for emergencies, retirement, or other goals can feel like an uphill battle.

- Managing Debt: Credit card balances and loans can become heavier burdens when you’re worried about your financial future.

- The Anxiety-Money Trap: The current economic climate, as suggested by your insights and echoed in articles like one from Psychology Today on financial anxiety, directly fuels financial stress. This isn’t just a fleeting worry; it deeply impacts mental health. Research from sources like the TIAA Institute and WorkRise Network consistently shows a strong, often bidirectional link: financial worries contribute to psychological distress (like anxiety and feelings of hopelessness), and poor mental health can, in turn, make it harder to manage finances effectively. Many Americans report feeling stressed about money, and this impacts sleep, self-esteem, and even productivity.

📊Section 3: Strategies for Improving Your Financial Literacy and Wellness in 2025

Okay, so we know it’s a tricky environment. But here’s the good news: you can absolutely take steps to improve your financial literacy and, by extension, your financial and mental wellness. Your insight is spot on: education and clear financial goals are crucial.

"An investment in knowledge pays the best interest."

- Benjamin Franklin Tweet

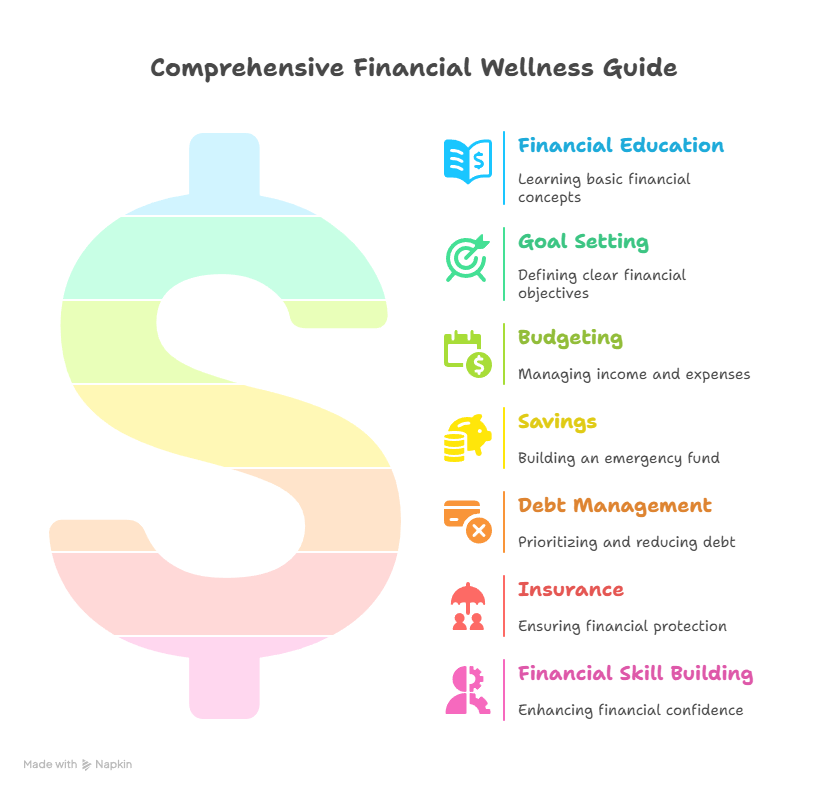

1️⃣Embrace Financial Education:

- Seek Knowledge: This is your starting point. Commit to learning. There are tons of resources available (more on that in the next section!). Understand basic concepts like budgeting, saving, debt, and investing. (more here: https://diyyourmoney.com/category/learnyourmoney/)

- Understand the “Why”: Don’t just learn how to budget; understand why it’s important for your peace of mind in 2025.

2️⃣Set Clear Financial Goals:

- Define Your Destination: In uncertain times, goals provide direction and a sense of control. What do you want to achieve? An emergency fund? Paying off a specific debt? Saving for a down payment?

- Make Them SMART: Specific, Measurable, Achievable, Relevant, Time-bound. Instead of “save more money,” try “save $50 from each paycheck for the next 6 months to build an emergency fund.” ( https://diyyourmoney.com/how-to-automate-personal-finance-in-2024/)

- Connect to Values: Why is this goal important to you? Security? Freedom? Peace of mind? Connecting goals to your values boosts motivation.

3️⃣Master Your Budget and Expenses:

- Track Your Spending: Know where your money is going. Use an app, a spreadsheet, or a notebook.

- Create a Realistic Budget: Plan how you’ll spend your money. Allocate funds for needs, wants, savings, and debt repayment. Be prepared to adjust it, especially with inflation (BECU offers tips on adjusting budgets for inflation).

- Identify Areas to Cut Back (if needed): Small changes can add up.

"A budget is telling your money where to go instead of wondering where it went."

- John C. Maxwell Tweet

4️⃣Build Your Savings:

- Emergency Fund is Key: Especially now! Aim for 3-6 months of essential living expenses in an easily accessible account. This cushions the blow of unexpected events, which is vital when recession fears loom (The Economic Times highlights the importance of an emergency fund).

- Save for Other Goals: Even small, regular contributions make a difference over time. Automate your savings if possible.

5️⃣Manage Debt Strategically:

- Prioritize High-Interest Debt: Tackle credit cards or loans with the highest interest rates first.

- Explore Repayment Options: If you’re struggling, contact your lenders to discuss hardship programs or alternative payment plans.

6️⃣Plan for the Unexpected (Beyond an Emergency Fund):

- Insurance Review: Ensure you have adequate health, disability, and (if needed) life insurance.

- Organize Documents: Keep important financial documents in a safe, accessible place.

7️⃣Build Financial Skill and Motivation:

- Practice Makes Progress: Regularly engage with your finances. Review your budget, track your goals, and make small, intentional decisions.

- Foster Financial Self-Efficacy: Believe in your ability to manage your money. Every small win – sticking to your budget for a week, saving an extra $20 – builds confidence.

- Limit Stressors: If constant news about the economy makes you anxious, limit your consumption. Focus on what you can control – your own financial actions.

📚Section 4: Resources and Support for Your Journey

You don’t have to do this alone! There are many organizations dedicated to helping you improve your financial literacy:

Government Agencies (USA):

- Consumer Financial Protection Bureau (CFPB): An invaluable resource (consumerfinance.gov) offering free tools, guides, and information on a vast range of financial topics, from debt collection to mortgages and saving. They also contribute to the Financial Literacy and Education Commission (MyMoney.gov).

- Federal Deposit Insurance Corporation (FDIC): Their Money Smart program provides financial education resources.

- Securities and Exchange Commission (SEC): Investor.gov has tools and resources for investors.

- Office of the Comptroller of the Currency (OCC): Provides a Financial Literacy Resource Directory.

Nonprofits:

- Organizations like the National Financial Educators Council (USA) and FLAB India (Financial Literacy Advisory Body India) offer workshops, counseling, online resources, and tailored programs. Many local community organizations also provide financial literacy support.

Others:

- Employers: Increasingly, companies are offering financial wellness programs as part of their benefits packages. Check what your employer might provide.

- Educational Institutions: Many colleges and even some schools are incorporating financial education into their curriculum. Online platforms also offer numerous courses.

🖲️Conclusion

The economic landscape of 2025 might feel a bit shaky, with valid concerns about governance, tariffs, inflation, and potential recessionary trends definitely contributing to feelings of anxiety. However, reacting with fear isn’t the answer; proactive education and planning are. Financial literacy is a vital tool for navigating these uncertainties, transforming anxiety into action, and fostering genuine financial wellness.

Understanding your money, setting clear goals, and knowing how to manage your resources effectively empowers you to build a more secure and less stressful future, regardless of the economic climate. It’s about taking control where you can, and that in itself is a huge step towards better mental well-being.

What’s your first step going to be?

- Will you draft a basic budget this week?

- Explore one of the resource websites mentioned?

- Set one small, achievable financial goal for the next month?

Share your thoughts, challenges, or your own favorite financial literacy tips in the comments below! Let’s learn and grow together.